企业作业预算管理研究

来源:wenku7.com 资料编号:WK77261 资料等级:★★★★★ %E8%B5%84%E6%96%99%E7%BC%96%E5%8F%B7%EF%BC%9AWK77261

以下是资料介绍,如需要完整的请充值下载。

1.无需注册登录,支付后按照提示操作即可获取该资料.

2.资料以网页介绍的为准,下载后不会有水印.资料仅供学习参考之用. 密 保 惠 帮助

资料介绍

企业作业预算管理研究(含开题报告,毕业论文11600字)

摘 要: 近些年,随着科学技术的快速发展,给传统的预算体系带来了巨大的冲击,传统的成本计算法显然已难以反映真实的成本信息,影响企业预算的科学性和可靠性,在这种情况下,构建新的作业预算管理模式,既是竞争环境发展的客观要求,也是对现在预算管理理论与方法的自我完善和发展。本文通过指出传统预算体系存在的缺陷,提出构建新的作业预算管理模式的要求,进而构建了作业预算管理模式并进行相关的研究;最后,列举企业在运用作业预算管理时应注意的问题。

关键词:作业预算;作业成本法;成本耗用

Study on Activity-Based Budgeting of Enterprise

Abstract:Recent years, with the rapid development of technology, the traditional budget system has incurred a huge impact, and the traditional method of cost calculation obviously has not reflected the true cost information, which affects the scientificity and reliability. In such a situation, constituting a new activity-based budget management model, is not only the objective requirement of the development of competition environments, but also the self-improvement and development of the present theory and method of the budget management.After pointing out existing definit of traditional budget system,this thesis makes dememds of building a new management mode of budget,then build it and make some relative researches.At last,list some matters needing of attention when enterprises use activity-based budgeting.

Key words: Activity-based budgeting;Activity-based costing;Cost depletion.

目 录

摘要……………………………………………………………………………………1

关键词…………………………………………………………………………………1

一、绪论………………………………………………………………………………2

(一)选题的意义………………………………………………………………2

(二)研究的目的………………………………………………………………2

(三)国内外研究现状…………………………………………………………2

1.关于国外企业作业预算的相关研究……………………………………2

2.关于国内作业预算管理的研究…………………………………………3

3.文献评述……………………………………………………………4

(四)本文的主要内容和研究方法…………………………………………4

(五)本文的研究的思路……………………………………………………5

二、传统预算管理的缺陷……………………………………………………………5

(一)编制基础不科学…………………………………………………………5

(二)预算编制周期设置不科学………………………………………………5

(三)难以发挥企业各部门之间的协调作用…………………………………6

(四)传统预算编制需要耗费很长时间………………………………………6

三、作业成本法与预算管理融合的可行性分析……………………………………6

(一)理论方面…………………………………………………………………6

(二)实践方面…………………………………………………………………7

1.作业成本法在企业预算管理中的运用…………………………………7

2.信息技术方面……………………………………………………………8

四、企业作业预算管理模式的构建…………………………………………………8

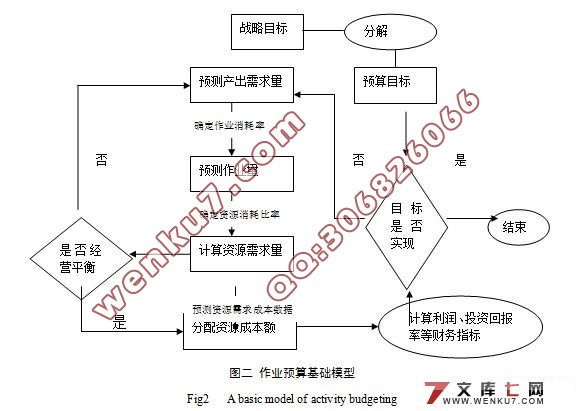

(一)作业预算的编制…………………………………………………………9

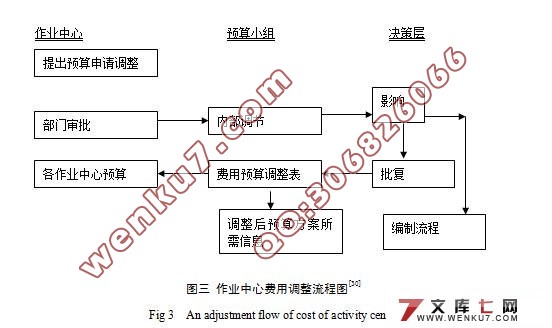

(二)作业预算的调整…………………………………………………………10

(三)作业预算的控制…………………………………………………………11

1.作业预算事前控制……………………………………………………11

2.作业预算事中控制……………………………………………………11

3.作业预算事后控制……………………………………………………12

(四)作业预算的绩效考核……………………………………………………13

1.作业预算业绩考核指标………………………………………………13

2.作业预算业绩考核的意义……………………………………………14

五、企业作业预算管理应注意的问题………………………………………………14

(一)必须与企业战略目标结合………………………………………………14

(二)划分作业中心时应考虑作业属性………………………………………14

(三)确定成本动因时应注意成本效益原则…………………………………14

六、结束语……………………………………………………………………………15

参考文献……………………………………………………………………………15

致谢…………………………………………………………………………………17

|